There’s nothing more American than debt.

We’re famous for it. China has jobs because of our debt.

Made in China. Borrowed and bought in America.

It’s the only thing more American than guns, beer, and freedom.

Well… and fraud.

Debt is owing money to people you’ve never met

for things you don’t even like anymore.

Like the treadmill.

A treadmill is just expensive proof that you hate going outside.

You’re literally paying money to walk and get nowhere.

It’s cardio with despair and a premium view of drywall.

Or the VR headset.

That’s not a better life.

That’s a different loading screen.

Which is Exactly What Debt is… The Appearance of a Better Life.

Because debt isn’t about having money.

It’s about looking like you have money.

Most people don’t actually own nice things.

They just rent them from the future.

You don’t own a house.

You have a loan.

You don’t own a truck.

You pay a monthly masculinity fee.

Big tires.

Big engine.

About a three-inch net worth.

I get it. I love trucks. I grew up in a small town.

When I bought my Raptor, my hometown friends told me it wasn’t a real truck.

My wealthy friends think I’m white trash.

At least it’s paid off and I actually like it.

That’s the part people skip.

We don’t buy things anymore.

That’s what people did in the 1950s when they handed over cash at the grocery store like cavemen.

Now we lease self-esteem.

We finance achievement.

It’s the same energy as renting a Ferrari and an Airbnb for Fakebook or Insta.

I call it a financial dick pick….because you have to be a dick to post a picture like that.

We Confuse Looking Rich with Being Rich.

America is one big costume party.

Everyone’s dressed as “successful.”

Especially on social media.

Especially now with AI.

Consumer debt isn’t intelligence.

It’s artificial money.

And borrowing to consume is very different than borrowing to create.

Because debt is based on money you’ll make later.

And when has “I’ll handle it later” ever worked out?

Later is when you’re tired.

Later is when you don’t want to work anymore, like an alcoholic’s liver.

Debt is money’s hangover.

Or herpes.

Because there’s no quick cure.

That’s Why Debt is Sold to the Young.

We’ve normalized it so much that paying interest feels like adulthood.

Like, “Congratulations, you’re responsible now. Here’s anxiety.”

We tell young people, “Stay out of debt and go to school.”

That’s like telling someone to hold their breath and run a marathon.

Or my favorite corporate line when I was asked to speak last year:

“Be yourself… just not offensive.”

Which is it?

And let’s talk about age restrictions for a second.

At 18 you’re a legal adult.

But you can’t drink.

You can’t rent a car.

You can’t gamble.

But here’s a 29% interest rate.

Roll the dice on your future.

You can go into debt before you can go into a bar.

I got my first credit card at 18 from a hot girl giving out free t-shirts.

Signed up for 22% interest.

Which was 22% more interest than she had in me.

And for too many kids, cards like that come with a complimentary lifetime of anxiety, intermittent fasting (by force and not choice), and living with your parents.

Young people don’t know.

They think energy is permanent.

They’ve never slept an injury. If you’re over 40, you know what I mean.

You wake up and something just… doesn’t work anymore.

Debt is sold to the young because they haven’t felt future pain yet. It’s like drinking without knowing the hangover is coming.

Debt is future work you haven’t agreed to yet.

The Problem Isn’t Debt. It’s Stupid Debt.

Here’s where it makes sense to slow down and think.

Debt isn’t the enemy.

Consumer debt is.

Debt that doesn’t pay you back.

Debt that feeds your ego more than your future.

Debt that creates stress instead of options.

The wealthy don’t fear debt.

They also don’t worship it.

They use it.

They leverage loans to buy assets, create cash flow, and increase optionality.

But they only do it when it aligns with who they are.

And this is where most advice fails.

Because personal finance isn’t universal.

It’s personal.

Some people would benefit most by paying off loans aggressively.

Others should absolutely keep their loans and invest.

The difference isn’t math.

It’s behavior.

It’s your mindset.

Your habits.

Your marriage.

Your risk.

Your ability to create value.

A 15-year mortgage might be great for a spender with no plan.

It might be disastrous for an entrepreneur in a growth phase.

A 50-year mortgage might be irresponsible for one person, but brilliant for another.

It depends.

That’s the part gurus hate saying.

I once watched Suze Orman tell a realtor with unpredictable income to refinance into a shorter loan so they could “pay it off faster.”

Don’t pay it off faster if it kills cash flow, and your cash flow isn’t predictable. An interest only loan would make more sense at that point, instead of an amortized loan. More flexible with payment and lowering payment with each dollar beyond the interest.

Stress is not a strategy.

One-size-fits-all advice ignores opportunity cost.

It ignores liquidity.

It ignores human behavior.

Fire can keep you warm.

Fire can also burn your house down.

Debt is the same way.

About That 10% Credit Card Cap…

Now we’re talking about capping credit card interest at 10%.

Sounds great emotionally.

But what changes behavior?

Lower interest doesn’t reduce prices.

It reduces payments.

It doesn’t fix inflation.

It doesn’t teach money psychology.

And it creates additional consequences.

If risk can’t be priced, credit tightens.

Limits get lowered.

Access disappears for those who may require the lifeline.

Banks don’t say “okay.”

They get creative.

Fees.

Requirements.

Reduced availability.

Capping rates doesn’t change spending habits.

It subsidizes them.

Debt gets cheaper.

Responsibility gets more expensive.

Some people will use the relief to recover.

Others will use it as permission to spend more.

Same story. Different chapter.

I don’t love 30% interest rates.

I also don’t eat at McDonald’s.

But I don’t want the government deciding what I’m allowed to eat either.

Freedom requires responsibility.

Responsibility requires knowledge.

There is a permanent penalty for financial ignorance.

You can outsource decisions to ‘big brother’

or you can build a bigger financial brain.

I choose knowledge over force.

Freedom over mandates.

The Real Question

Debt isn’t sinful.

Debt isn’t salvation.

It’s leverage.

And leverage in the hands of someone who doesn’t understand it

is just a club you use to hit yourself in the head.

So where do you stand?

What kind of loans affect your sleep?

Your marriage?

Your creativity?

Are you borrowing to consume or to create?

Are you buying relief or building capacity?

If this made you uncomfortable, good.

That’s the sound of a financial sacred cow on the way to the slaughterhouse.

To your prosperity,

Garrett

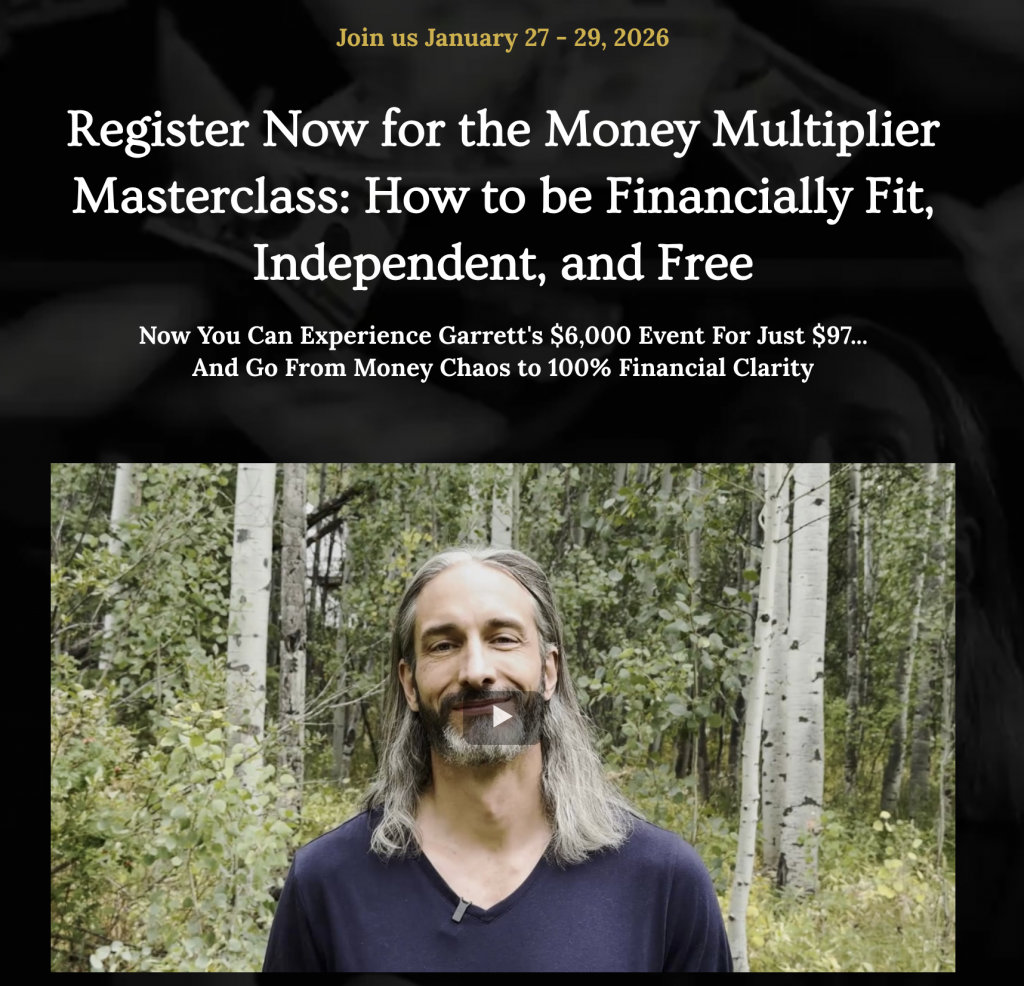

P.S. My next Money Multiplier Masterclass is coming January 27th–29th!

Our last Masterclass was a hit. We got amazing feedback. I had a blast sharing my message with passion. And we even built a fun, collaborative community with VIP members in a private WhatsApp group. Tickets are on sale now for just $97.

Join us, and go from money chaos to financial clarity.

Ready to Stop Guessing With Your Money?

Most financial advice tells you to save more and spend less. That’s a losing game. Garrett’s free book Killing Sacred Cows reveals why the conventional wisdom is costing you—and what to do instead.

Do it yourself? Try the free Relationship Currency tool on X1 Wealth.

Frequently Asked Questions

Is all debt bad in America?

No. The problem isn’t debt itself—it’s owing money for things you don’t value or that don’t create value. Productive debt that builds assets or cash flow is a tool. Consumer debt for treadmills and VR headsets is just expensive regret.

What’s the difference between good debt and bad debt?

Good debt produces income, appreciates, or creates leverage. Bad debt is money you owe for things you don’t even like anymore—the treadmill, the forgotten subscription, the impulse buy gathering dust.

Should I avoid all debt to be financially free?

Not if you want to build wealth. Avoiding all debt is like avoiding all risk—it sounds safe, but it keeps you small. The wealthy use debt strategically. The broke use it emotionally.

Why do Americans have so much consumer debt?

Because we’ve been sold the idea that lifestyle equals success. We borrow for proof of status instead of investing in assets that produce. It’s expensive theater, and most people are playing a role they can’t afford.